Disclosure: “The owners of this website may be paid to recommend Goldco or other companies. The content on this website, including any positive reviews of Goldco and other reviews, may not be neutral or independent.” Learn More

Most gold companies want to lock your metal in a vault and never let you touch it. Glint Pay flips that idea: buy real gold, then spend it on groceries with a debit card.

That premise sounds either brilliant or too good to be true, which is exactly why I dug into this Glint Pay review.

I wanted to know if a retirement saver could trust it, what it actually costs, and whether the gold you buy really exists. Here’s what the research shows.

Table of Contents

- 1 What Is Glint Pay?

- 2 How Does Glint Pay Work?

- 3 Glint Fees: The Complete Breakdown

- 4 Is Glint Pay Safe? What’s Insured and What Isn’t

- 5 The 2019 Insolvency: What Actually Happens If Glint Fails

- 6 Can You Verify Your Gold Exists? Audits and Transparency

- 7 The Tax Problem With Spending Gold (US)

- 8 What Real Users Say (Trustpilot, App Store, Google Play)

- 9 Glint vs. the Alternatives

- 10 Who Should (and Shouldn’t) Use Glint

- 11 How to Open a Glint Account (5 Steps)

- 12 Frequently Asked Questions

- 12.1 Q1. Is Glint Pay Legit?

- 12.2 Q2. Is Glint FDIC Insured?

- 12.3 Q3. Is Glint a Bank?

- 12.4 Q4. What Happens to My Gold If Glint Goes Bust?

- 12.5 Q5. Can I Take Physical Delivery of My Gold?

- 12.6 Q6. Does Glint Report to the IRS / Do I Owe Taxes When I Spend Gold?

- 12.7 Q7. What Countries Is Glint Available In?

- 12.8 Q8. How Long Do Glint Withdrawals Take?

- 12.9 Q9. Does Glint Support Silver?

- 12.10 Q10. How Does Glint Make Money?

- 13 Verdict

What Is Glint Pay?

Glint Pay is a fintech app paired with a prepaid Mastercard that lets you buy, hold, and spend physical gold and silver as if it were cash.

Founded in 2015 and headquartered in London with a US entity based in Boulder, Colorado, the company was created by Jason Cozens after the 2008 financial crisis pushed him to build an alternative to fiat money.

The platform reports more than 246,000 registered users and over $574 million in bullion stored on behalf of customers. It is regulated as an electronic money institution in the UK and operates as a card program manager in the US.

Glint is a payments and savings tool built on allocated gold. It is a technology company, not a bank.

Who’s Behind Glint

Jason Cozens remains CEO today, bringing two decades of experience in eCommerce and digital businesses, including the online bullion dealer GoldMadeSimple.com.

Glint has raised roughly $26.8 million across nine funding rounds, with backers including Sprott Asset Management, a well-known name in precious metals investing.

The UK entity is an FCA-authorized electronic money institution, which means it must follow strict rules on safeguarding customer money. The US entity acts as a card program manager, partnering with Sutton Bank to hold dollar balances.

The board carries real weight. It includes Haruko Fukuda OBE, former CEO of the World Gold Council, and Oliver Bolitho, former Chairman of Goldman Sachs Asset Management Asia. That level of experience matters for a company asking you to store bullion with it.

What Glint Is Not

Glint gets confused with three things it is not, so let me draw clear lines:

- It is not a bank. Your gold is not a deposit, and Glint does not lend your money out.

- It is not an ETF. You own allocated physical bullion, not shares in a fund that tracks gold’s price.

- It is not a gold-backed crypto token. There is no blockchain, no coin, and no digital wrapper between you and the metal.

Each ounce in your account matches an ounce of real gold sitting in a vault. That is the whole pitch.

How Does Glint Pay Work?

Glint Pay revolutionizes monetary transactions by reintegrating gold into everyday financial activities. This innovative approach offers a significant advantage in an economy where traditional currency faces devaluation through inflation and market fluctuations.

The platform combines traditional gold ownership with modern convenience, enabling users to purchase, store, transfer, and utilize gold as currency. Through their integrated app and Glint Mastercard®, the system provides seamless financial management.

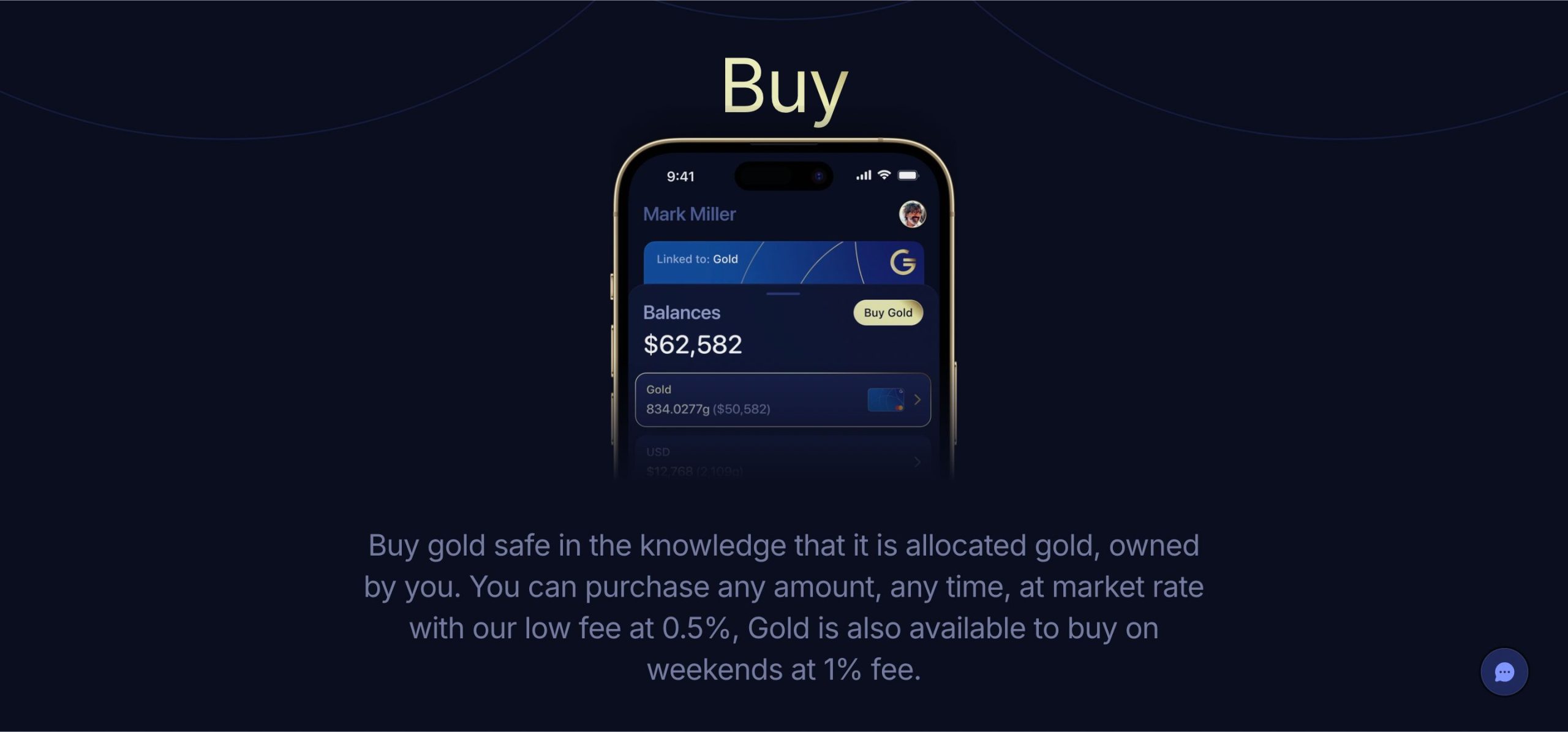

Buying Gold and Silver

When you buy through Glint, you get allocated ownership at wholesale market rates plus a 0.9% fee.

You can buy fractional amounts starting from as little as a penny, so there is no large minimum blocking new savers. Your metal sits in a Brink’s vault in Switzerland, insured through Lloyd’s of London.

Glint also supports silver, which many older competitor reviews miss. Holdings are 99.99% purity and independently audited by Bureau Veritas.

The word “allocated” is the important part. It means specific bullion belongs to you, not a paper claim shared across thousands of customers.

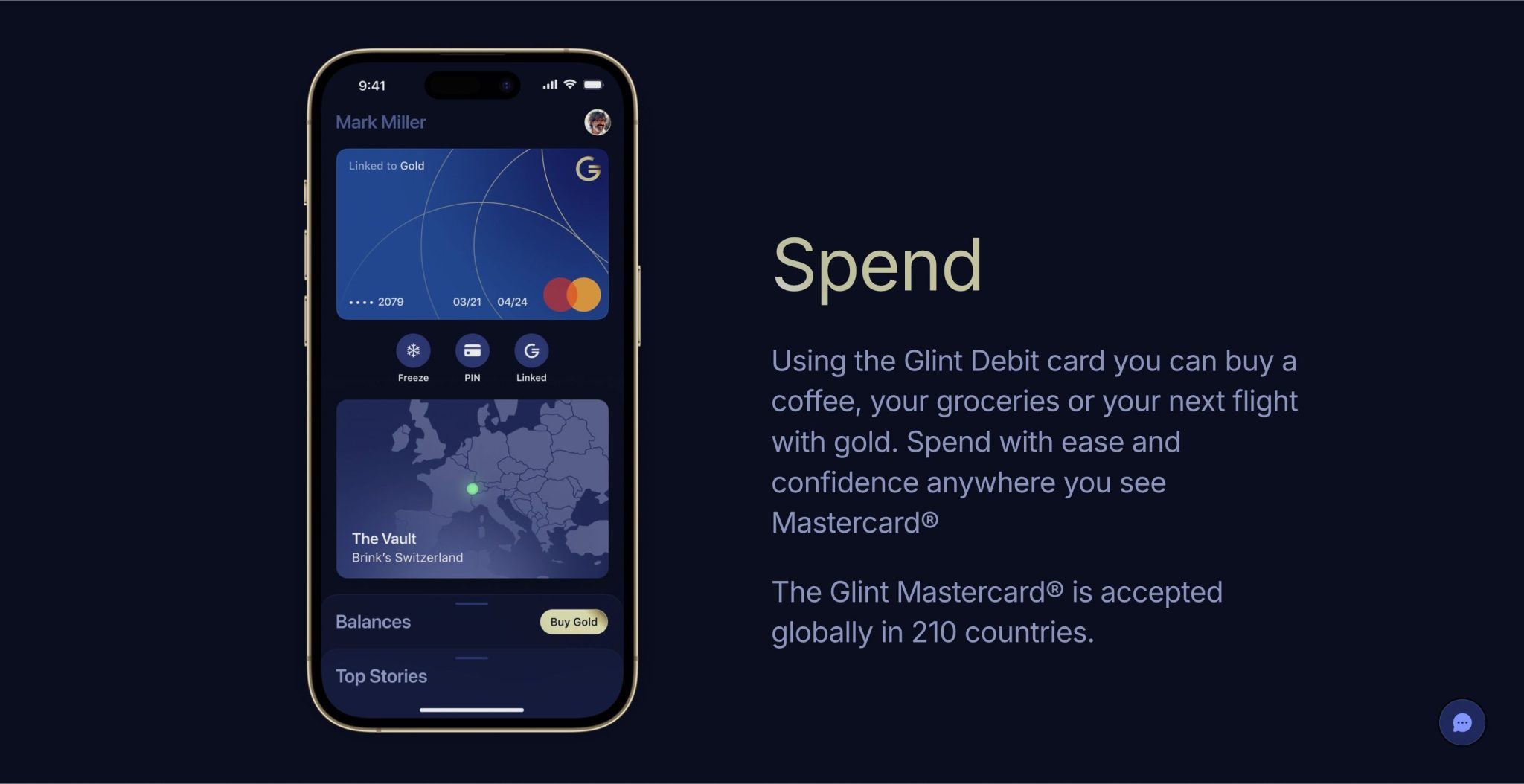

Spending Gold With the Glint Mastercard

Here is where Glint earns its name. Say you swipe the card for a $40 dinner. At that exact moment, Glint sells $40 worth of your gold at the live spot rate, converts it to dollars, and pays the merchant. The whole thing takes seconds.

Key spending facts:

- Accepted in 210 countries and territories wherever Mastercard works.

- Daily spend limit of $5,000, with a monthly cap of $50,000.

- ATM withdrawals are capped at roughly $310 per day.

You choose whether each purchase draws from your gold, silver, or dollar wallet, which gives you control over when you actually sell metal.

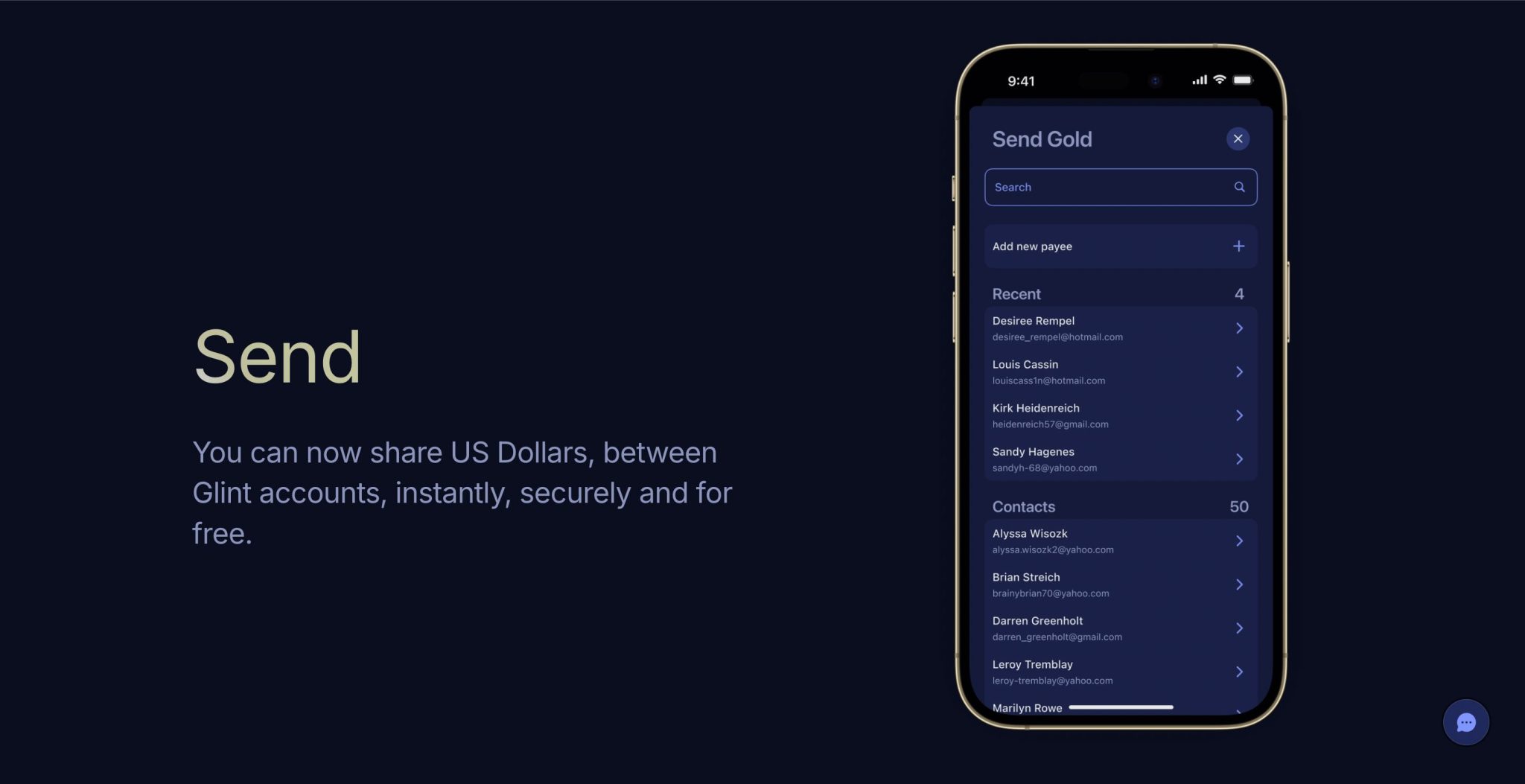

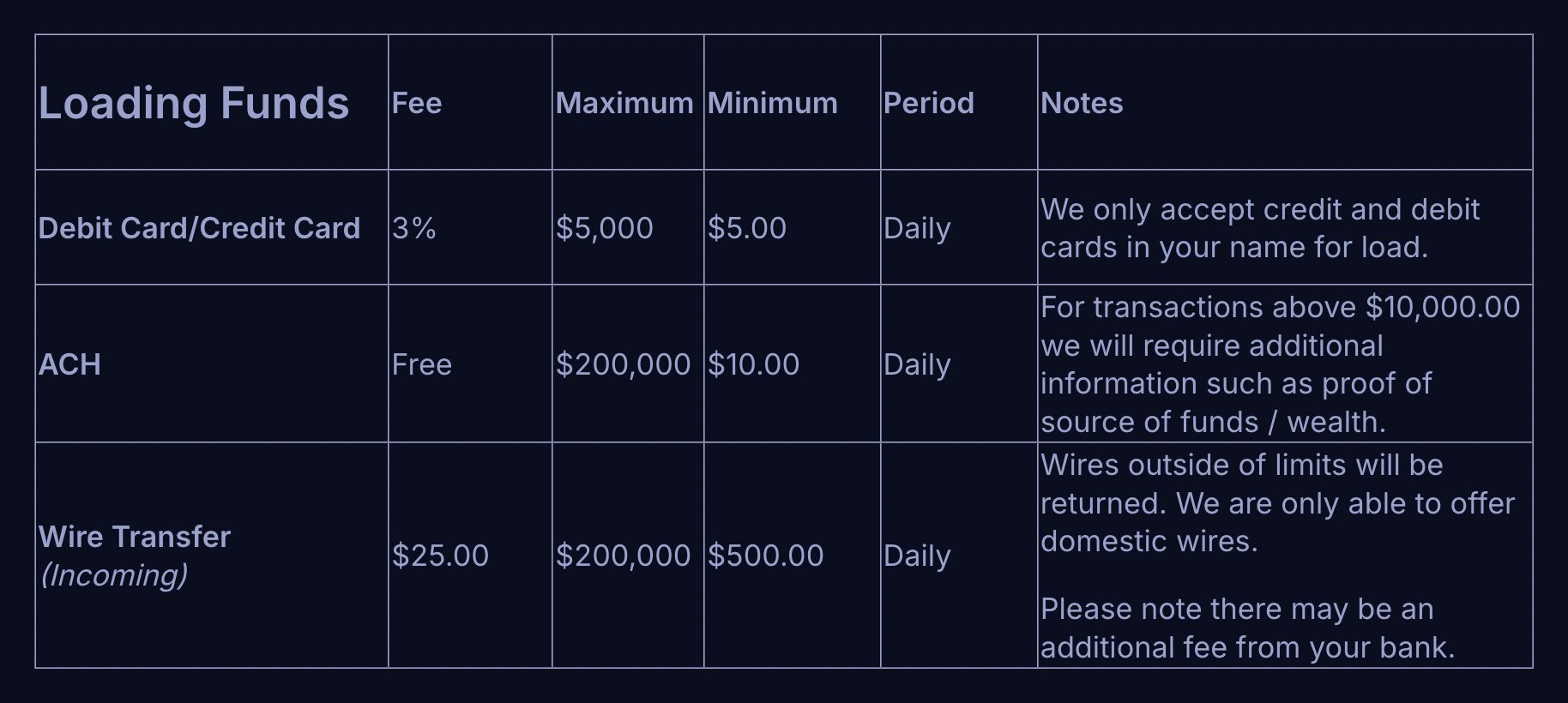

Holding and Transferring USD

Your dollar balance sits in an FDIC-insured account at Sutton Bank, a member of the FDIC. Sending dollars between Glint accounts is free and instant, which makes splitting a bill or paying a family member simple.

One honest sticking point: when you sell gold back to cash, it can take around three business days for funds to settle in your wallet.

Users mention this delay often, and it matters if you want to react fast during a volatile market. Plan around it rather than expecting instant liquidity.

Glint Fees: The Complete Breakdown

Glint’s headline fees look reasonable, but the full picture includes storage, spreads, and taxes. Let me lay it all out.

Trading and Storage Fees

Here are the core costs, verified against Glint’s published schedule effective May 1, 2025:

- Buy fee: 0.9% on gold and silver.

- Sell fee: 0.9% on gold and silver.

- Gold storage and insurance: 0.02% monthly, roughly 0.24% per year, with a $1 minimum.

- Silver storage and insurance: 0.04% monthly, roughly 0.48% per year, with a $2 minimum.

- Account closure: free.

Always confirm current rates in the app, since fee schedules change. This breakdown reflects the May 2025 numbers.

Card and Spending Fees

Spending costs depend on how you use the card:

- Domestic USD card payments: free up to $5,000 per day.

- Gold-funded or international payments: 0.9%.

- ATM withdrawals: $1.50 each, with a $310 daily limit.

- Card replacement: $5; standard delivery $10, taking up to 10 working days.

For a traveler, that 0.9% international rate beats the 3% many debit cards charge abroad. That single difference can justify the card for frequent flyers.

The Fees Glint Doesn’t List

Some costs never appear on a fee page:

- The spread between the buy and sell price at execution eats into value every time you trade.

- The three-day sell settlement is an opportunity cost, since your money sits idle while gold prices move.

- Taxes are the invisible expense most people forget. More on that in the tax section below.

These hidden costs rarely show up in marketing, so factor them in before you commit.

What $1,000 in Glint Costs in Year One

Let me run a simple example. You deposit $1,000 by ACH (free), then buy $1,000 of gold at the 0.9% fee, costing $9. You hold it for a full year, paying about 0.24% storage, roughly $2.40. If you sell it all at year-end, that is another 0.9%, or about $9.

Your total first-year cost on a buy-hold-sell cycle is roughly $20.40, or about 2%. If you only buy and hold without selling, your cost drops closer to $11.40.

Is Glint Pay Safe? What’s Insured and What Isn’t

Yes, Glint uses regulated custody, segregated accounts, and vault insurance, but not every part of your balance carries the same protection.

This is where most reviews get sloppy. I will separate protection into three clear buckets, because blurring them is how people get misled.

Glint’s own App Store disclaimer states plainly that precious metals are “NOT FDIC INSURED, NOT DEPOSITS, AND MAY LOSE VALUE.” That honesty against its own marketing is a good sign.

Your US Dollars: FDIC-Insured via Sutton Bank

The cash in your USD wallet is protected up to $250,000 through Sutton Bank, an FDIC member. This coverage applies only to dollars, not to any metal you hold. If Glint failed, your dollar balance would carry the same federal backstop as a normal bank account.

Your Gold: Allocated, Vaulted, Lloyd’s-Insured

Your bullion is allocated to you and stored at Brink’s, with insurance through Lloyd’s of London. That insurance covers physical risks like theft or loss inside the vault.

It does not cover price drops. If gold falls 20%, your insurance does nothing. It also does not act like FDIC coverage against company failure.

The Company: Safeguarding, Not Deposit Insurance

Under FCA rules, Glint must keep customer money in segregated accounts separate from its own funds. This is called safeguarding, and it is different from deposit insurance.

There is no FSCS protection for your gold in the UK, and no equivalent government scheme covering the metal. Safeguarding means your assets are ring-fenced, which sets up why the 2019 episode matters.

Account and App Security

On the personal level, Glint applies:

- KYC identity checks at signup.

- The ability to freeze or cancel your card instantly in the app.

- Fraud monitoring on transactions.

Like any digital platform, it carries data-breach exposure, so use a strong password and enable every security feature offered.

The 2019 Insolvency: What Actually Happens If Glint Fails

Here is the part almost no competitor review will tell you. In 2019, Glint went into administration. That sounds alarming, but the outcome is actually reassuring evidence that the safeguarding model works.

What Happened in 2019

In September 2019, shortly after a funding round and its US launch, Glint entered administration. FRP Advisory was appointed as administrator, and a dispute with a secured creditor triggered the process.

The FCA issued a customer notice during the period. Administrators confirmed a full reconciliation of customer funds, meaning the gold customers owned was accounted for and protected.

How Glint Was Rescued

By November 2019, management and investors rescued the company with a £5.7 million injection. Glint relaunched and kept operating.

The recovery was real. During the early COVID period, Glint reported a purchase spike of around 700% as investors rushed to gold. The company survived its worst moment and grew afterward.

What Would Happen to Your Money Today

If Glint failed now, here is the priority structure:

- Customers rank ahead of all creditors except administrator costs under safeguarding rules.

- There is no FSCS or government backstop specifically for your gold.

- On the US side, your dollar wallet keeps its FDIC coverage through Sutton Bank.

The 2019 test showed customer assets stayed intact. That track record is more useful than any marketing promise.

Can You Verify Your Gold Exists? Audits and Transparency

Trust in a gold platform comes down to one question: does the metal really exist? Glint gives you tools to check, though its public transparency has room to improve.

What “Legally Allocated” and “Constructive Possession” Actually Mean

Legally allocated means specific, identifiable bullion is titled to you, not pooled with other people’s holdings. You own that exact metal.

Constructive possession means you have legal ownership and the right to take physical delivery, even though the gold physically sits in a vault. In plain terms, it is yours even when you cannot touch it.

Glint’s Audit Policy: Daily Reconciliation, Quarterly Audits, No Public Reports

Glint reconciles holdings daily and conducts independent audits quarterly through Bureau Veritas. Support has stated that a client-facing verification tool is planned, though it is not live yet.

The gap here is that Glint does not publish audit reports for customers to read directly. You have to trust the process rather than inspect it.

How Competitors Handle Proof of Reserves

Some rivals go further on public transparency:

| Platform | Public audit reports |

| Glint Pay | Quarterly audits, not published publicly |

| Kinesis Money | Publishes proof-of-reserves data |

| OneGold | Backed by APMEX/Sprott with published reporting |

If public proof-of-reserves is your top priority, competitors currently lead on this point.

How to Verify Your Own Holdings

You have two practical options:

- Request physical delivery of your gold, which confirms it exists (though fees apply, and the minimum redemption is 10 grams).

- Email Glint support directly and ask for confirmation of your allocated holdings and the vault audit schedule.

Sending that email is the simplest way to test the company’s responsiveness before you commit serious money.

The Tax Problem With Spending Gold (US)

Here is the catch nobody puts on a billboard. In the US, every time you spend gold, you trigger a taxable disposal of a collectible. This is the single most overlooked issue with the whole “gold as money” idea.

Why Buying a Coffee With Gold Is a Taxable Event

Say you buy gold at $2,000 per ounce. A week later, gold rises to $2,100, and you swipe your card for a $5 coffee. You just sold a tiny slice of gold that had gained value.

That means you realized a small capital gain on that $5 purchase. The IRS treats each sale as a reportable event, no matter how small.

Short-Term vs Long-Term Rates on Gold

If you held the gold less than a year, gains are taxed as ordinary income at your regular rate. That can reach the high tens of percent depending on your bracket.

If you held it more than a year, gold counts as a collectible, and long-term gains are capped at 28%, higher than the 15-20% on stocks. Either way, gold carries a heavier tax load than typical investments.

The Record-Keeping Burden for Daily Spenders

A daily spender could generate hundreds of micro-lots per year, each with its own cost basis. Glint’s statements provide transaction records, but they do not file your taxes or fully calculate every lot for you.

This burden mostly hits people who use the card constantly. Buy-and-hold users who rarely spend largely sidestep the mess. Talk to a CPA before treating gold like a checking account.

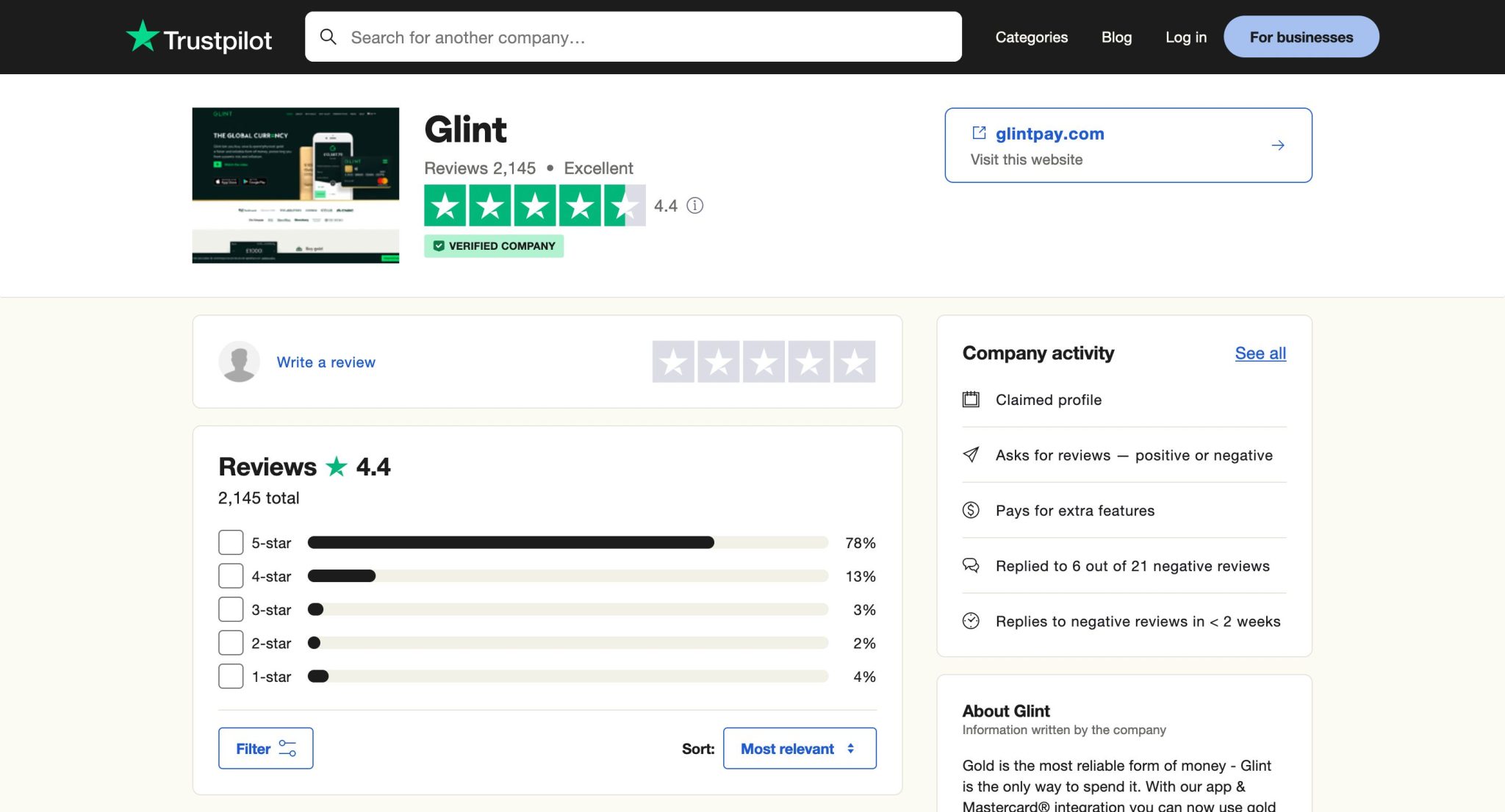

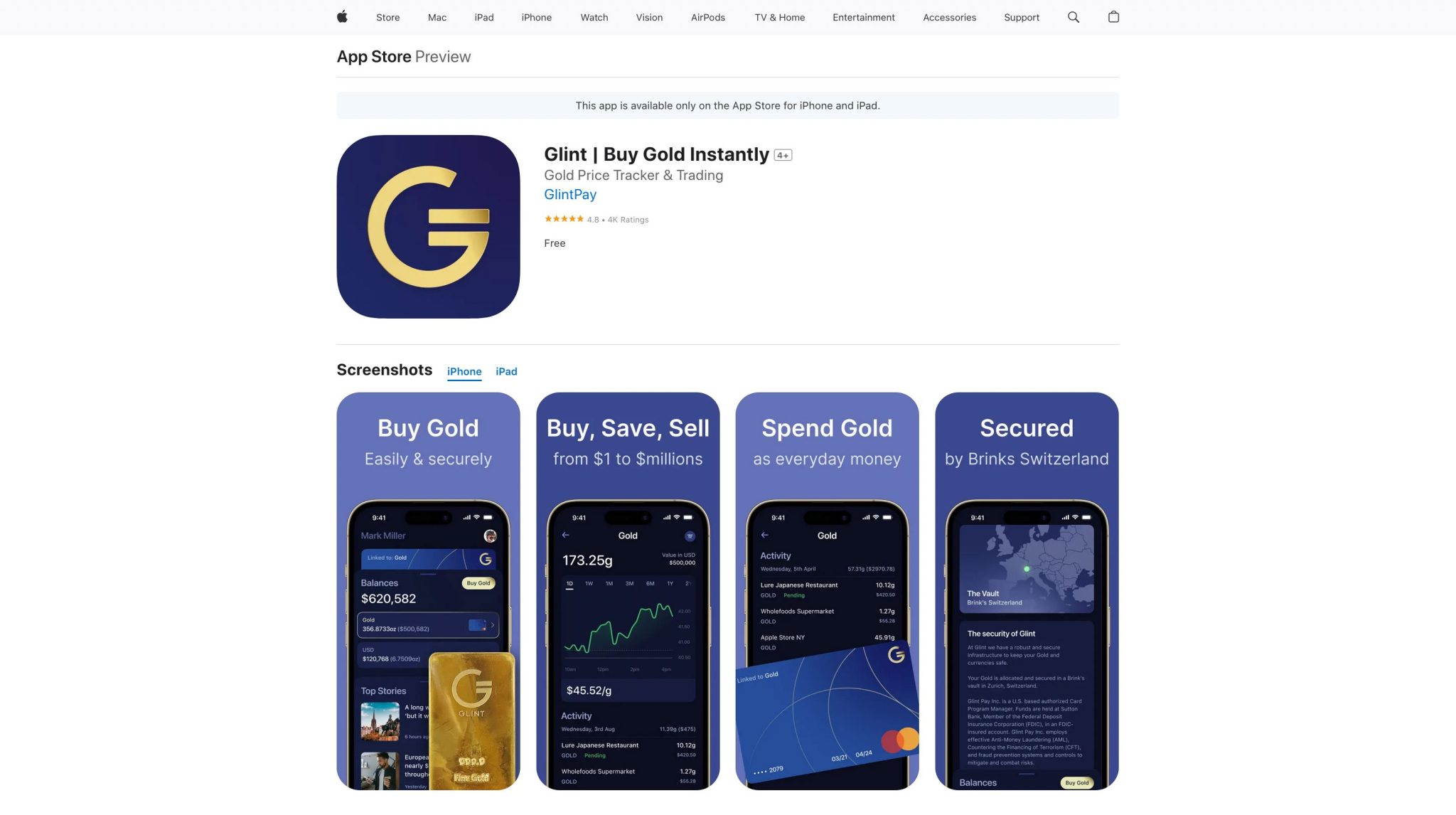

What Real Users Say (Trustpilot, App Store, Google Play)

Rather than cherry-pick glowing quotes, here is the honest consensus across major review platforms.

The Consensus Rating

- Trustpilot: 4.5 out of 5 across more than 2,827 reviews.

- Apple App Store: 4.8 out of 5 from about 4,600 ratings.

- Google Play: 4.4 out of 5 from roughly 2,180 reviews.

These figures were checked at the time of writing and can shift, so glance at current numbers before deciding.

What Users Consistently Praise

Three themes come up again and again:

- Signup and identity verification are quick and painless.

- The app is clean, easy to read, and simple to use.

- Buying gold and silver feels straightforward, with low premiums compared to pawn-shop markups.

Several long-term users report strong satisfaction, with one saying his balance more than doubled over three years thanks to rising gold prices.

The Recurring Complaints

The negative reviews cluster around specific issues:

- The three-day settlement delay after selling metal frustrates users who want fast access to cash.

- Some report login errors, especially during busy market moments.

- Certain top-up cards get rejected, forcing users to fund by bank transfer.

- A few describe activation or verification friction at signup.

Support replies to 98% of negative Trustpilot reviews, usually within two weeks, which shows the company engages rather than hides.

Glint vs. the Alternatives

No single platform wins for everyone. Here is how Glint stacks up against the real options.

| Feature | Glint | Kinesis | OneGold | Vaulted | Gold ETF + travel card |

| Spendable card | Yes | Yes | No | No | Visa Card |

| Published audits | No | Yes | Yes | Varies | Fund audited |

| Silver support | Yes | Yes | Yes | Limited | Some ETFs |

| Storage Cost | ~0.24%/yr | Low | Low | Low | Fund fee |

Glint vs. Kinesis

Both let you spend metal. Kinesis publishes proof-of-reserves and even pays yields on holdings, which Glint does not.

Kinesis appeals to transparency-focused users, while Glint offers a smoother card experience and broader consumer polish. If audits matter most, Kinesis leads; if ease of use wins, Glint edges ahead.

Glint vs. OneGold

OneGold carries the backing of APMEX and Sprott, both major names in bullion. It offers strong reporting but has no spendable card.

OneGold suits pure investors who want reputable custody, while Glint suits people who want to actually spend their metal.

Glint vs. Vaulted

Vaulted offers cheaper storage and physical delivery of Royal Canadian Mint gold, but it has no card and no spend feature. Choose Vaulted for low-cost long-term storage; choose Glint if spending flexibility drives your decision.

Glint vs a Plain Gold ETF Plus a Travel Card

Here is the comparison nobody else makes. You could buy a gold ETF in a brokerage account at a fraction of a percent per year and carry a low-fee travel card for spending.

That combo is cheaper for pure investing but loses the direct physical ownership and the seamless gold-to-spend link. Glint bundles both into one app, and you pay for that convenience.

Who Should (and Shouldn’t) Use Glint

No single platform fits every saver, so match Glint against your own habits and goals before opening an account.

Glint Is a Good Fit If…

- You want an inflation hedge that you can actually spend, not just store.

- You travel internationally and want to beat typical 3% debit card foreign fees with Glint’s 0.9%.

- You are a small-balance gold buyer who values having no minimum purchase.

These users get real utility from combining savings and spending in one place.

Skip Glint If…

- You are a buy-and-hold investor who would pay less through a low-fee vaulting service or a gold ETF.

- You spend daily and refuse to track dozens of taxable gold lots each year.

- You want FSCS or SIPC-style protection specifically covering your metal.

For those people, cheaper or better-protected options exist elsewhere.

How to Open a Glint Account (5 Steps)

Setting up Glint takes only a few minutes on your phone, and the five steps below walk you through the whole process from download to first purchase.

Step 1 — Download the App and Register

Glint works only on iOS and Android. There is no desktop version, so you must use a phone or tablet to open and manage your account.

Step 2 — Verify Your Identity

You submit a photo ID and a selfie for KYC checks. Approval is usually quick, though busy periods can add delay.

Step 3 — Fund Your Account

You can fund by bank transfer or debit/credit card. Card top-ups sometimes fail, based on user reviews, so ACH bank transfer is the more reliable route despite taking a few days to clear.

Step 4 — Buy Gold or Silver

Once funded, you buy metal at live rates plus the 0.9% fee. Fractional purchases start from a penny, so you can test the process with a tiny amount first.

Step 5 — Activate Your Glint Mastercard

The card arrives by mail, and you activate it in the app. Some users report activation friction, so contact support if it stalls rather than assuming it failed.

Frequently Asked Questions

Q1. Is Glint Pay Legit?

Yes. Glint is a registered, FCA-authorized electronic money institution in the UK with a US card program and over 246,000 users. It survived a 2019 administration with customer funds intact.

Q2. Is Glint FDIC Insured?

Partially. Your USD wallet is FDIC-insured up to $250,000 through Sutton Bank. Your gold and silver are not FDIC-insured and may lose value.

Q3. Is Glint a Bank?

No. Glint is a fintech app and prepaid Mastercard program. It does not take deposits or lend money like a bank does.

Q4. What Happens to My Gold If Glint Goes Bust?

Your allocated gold stays yours under safeguarding rules, ranking ahead of creditors except administrator costs. The 2019 administration confirmed customer funds were fully accounted for.

Q5. Can I Take Physical Delivery of My Gold?

Yes. The minimum redemption is 10 grams, arranged through Glint support. Fabrication and delivery fees apply, since vaults hold large bars.

Q6. Does Glint Report to the IRS / Do I Owe Taxes When I Spend Gold?

Spending gold is a taxable disposal in the US. Each sale can trigger a capital gain on a collectible. Keep records and consult a CPA.

Q7. What Countries Is Glint Available In?

The Glint Mastercard works in 210 countries and territories wherever Mastercard is accepted. Account availability depends on your region of residence.

Q8. How Long Do Glint Withdrawals Take?

USD withdrawals by ACH are free and typically clear within a few days. Selling gold to cash can take around three business days to settle.

Q9. Does Glint Support Silver?

Yes. Glint supports both gold and silver, stored in Brink’s vaults and insured through Lloyd’s of London.

Q10. How Does Glint Make Money?

Glint earns from the 0.9% buy and sell fees, monthly storage and insurance charges, card fees, and margins on out-of-hours trading.

Verdict

Glint Pay is a legitimate, regulated way to own physical gold and spend it like cash, best suited for inflation-conscious savers and international travelers who value flexibility over rock-bottom cost.

Its 2019 survival, FDIC-covered dollar wallet, and allocated Brink’s storage build real trust, though the three-day sell settlement, US tax friction, and lack of public audits are honest drawbacks.

I rate it 4 out of 5 for the right user. This review was compiled by studying Glint’s published fees, regulatory filings, and thousands of user reviews across Trustpilot, Apple, and Google Play, verified at the time of writing.

Goldco Precious Metals

- Goldco Surpasses $2 Billion in Precious Metals Placements

- Over 6,000 Five-Star Ratings on BBB, Trustpilot, and ConsumerAffairs

- Seven-Time Winer on the Inc. 5000 List