Disclosure: “The owners of this website may be paid to recommend Goldco or other companies. The content on this website, including any positive reviews of Goldco and other reviews, may not be neutral or independent.” Learn More

Gold sitting in a vault you’ll never touch, run by a company that changed hands and quietly rewrote its fee schedule. That’s the tension every prospective buyer runs into.

I spent days digging through official filings, fee documents, and hundreds of customer reviews to answer one question: can you trust this platform with your retirement savings?

I started this Goldmoney review because a friend nearing retirement asked me point-blank whether he should move part of his nest egg into allocated bullion here. The answer turned out to be more complicated than a simple yes or no.

Table of Contents

- 1 My Verdict Up Front

- 2 The Story Behind Goldmoney

- 3 What You’re Actually Buying Into

- 4 Getting Started: Account Setup and Verification

- 5 Funding, Buying, and Payment Methods

- 6 Where Your Metal Lives: Vaults and Custody Partners

- 7 Breaking Down the Real Cost of Goldmoney

- 8 Cashing Out: Selling, Withdrawing, and Taking Delivery

- 9 Keeping Your Assets Safe

- 10 What Real Customers Are Saying

- 11 The Case For and Against Goldmoney

- 12 Who Should and Shouldn’t Use Goldmoney

- 13 Frequently Asked Questions

- 13.1 Q1. Is Goldmoney Safe to Store Thousands of Dollars of Gold With?

- 13.2 Q2. Why Did My Goldmoney Account Get Flagged for Re-Verification When I Tried to Withdraw?

- 13.3 Q3. Does Goldmoney Actually Charge Only 0.5% When I Sell, or Is It More?

- 13.4 Q4. Can I Take Physical Possession of the Gold I Buy on Goldmoney?

- 13.5 Q5. Why Do Goldmoney’s Ratings Differ So Much Between Trustpilot and Sitejabber?

- 14 My Final Take

My Verdict Up Front

Goldmoney is a real, publicly traded company that has stored physical metal for over two decades. It is not a scam. I’d give it roughly 3.5 out of 5.

The platform genuinely holds allocated, insured bullion in named vaults, and the buy-in costs sit below most gold ETFs. For a mid-to-large holder who wants low-cost custody and plans to leave metal parked for years, it works.

But I would not call it perfect. The monthly storage minimum punishes small balances, the re-verification process frustrates people trying to withdraw, and the 2016 ownership change soured a chunk of long-time customers.

If you go in knowing the fee traps, it’s a reasonable choice. If you expect a coin dealer that ships bars to your door cheaply, look elsewhere.

The Story Behind Goldmoney

To judge whether a custody firm deserves your trust, you have to know who built it and who runs it now. Goldmoney’s history has two distinct chapters, and the break between them explains most of the complaints you’ll read online.

From James Turk to Roy Sebag: The Ownership Shift That Changed Everything

The original GoldMoney launched in 2001 out of Jersey in the Channel Islands. Its founder, James Turk, was a former Chase Manhattan analyst who pioneered the idea of “digital gold currency,” letting people hold allocated bullion through an online account long before that was common.

Then things shifted. In 2014, a Toronto startup called BitGold was founded by Roy Sebag and Josh Crumb. BitGold went public on the TSX Venture exchange in May 2015 and, in the same year, bought the original GoldMoney for around $52 million.

By 2016 the combined firm took the Goldmoney Inc. name and also picked up SchiffGold, a US retail bullion dealer. Roy Sebag became Chairman and CEO, a role he still holds.

Here’s why this matters to you. Many customers who joined during the “James Turk era” say the terms they signed up under changed after Sebag took over.

New storage fees appeared on accounts that once had none, and policy updates were, in their words, poorly communicated. If you read a bitter one-star review complaining about “changes,” it almost always traces back to this handover.

Where the Company Stands Today

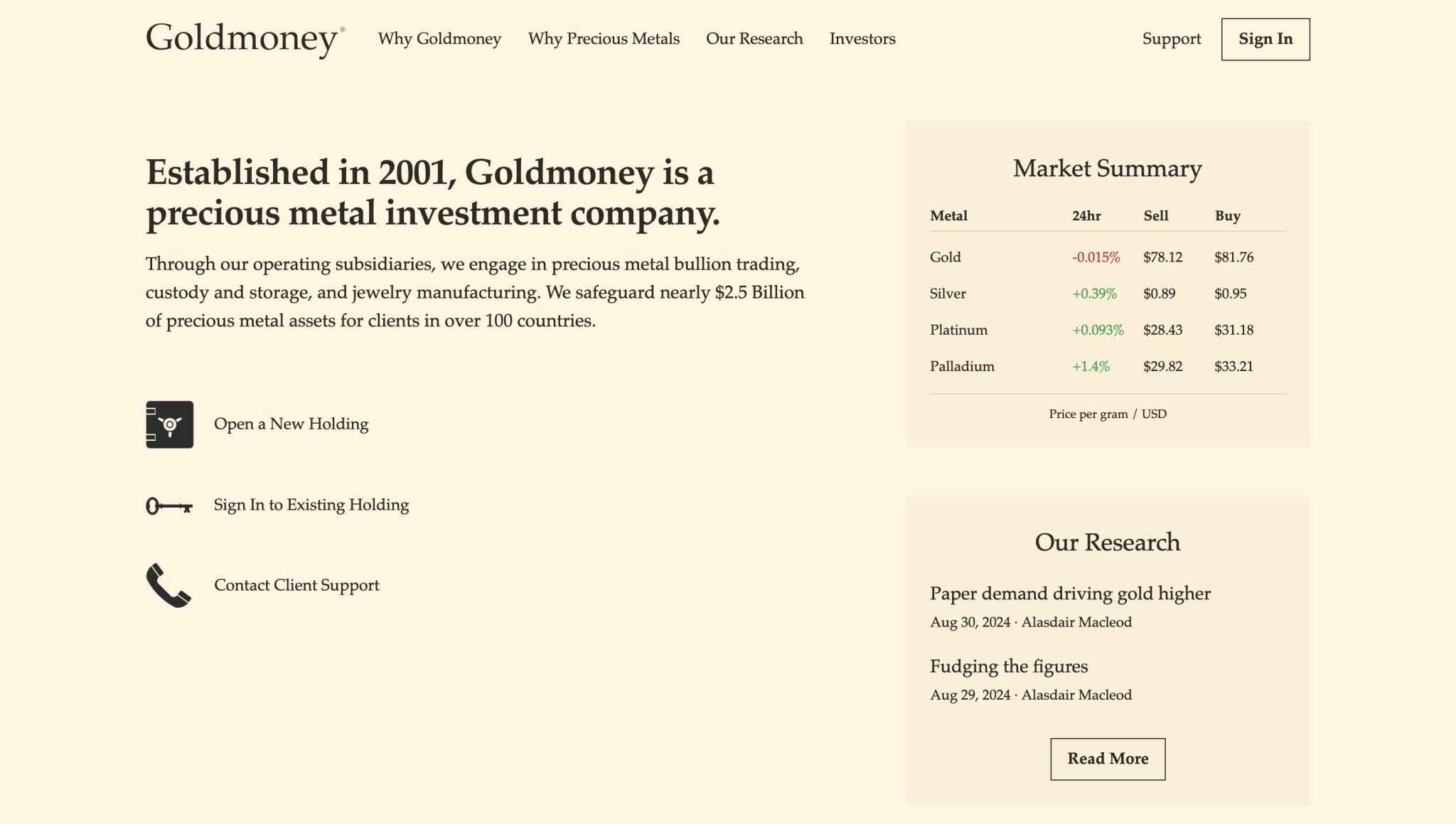

Today Goldmoney trades on the Toronto Stock Exchange under the ticker XAU (and XAUMF in the US). Public listing means it files audited financials and answers to regulators, which is more transparency than most private bullion dealers offer.

The company reports safeguarding close to $5 billion in precious-metal assets for people in more than 100 countries. Its development team works out of Milan, its headquarters sit in Toronto, and corporate filings are datelined in the British Virgin Islands.

Founders and board members own roughly 42% of shares, and the firm carries no debt. You can confirm the listing details on the TMX exchange site.

What You’re Actually Buying Into

Before you fund anything, get clear on the product. Goldmoney is not a coin shop and not a paper certificate. It’s a custody account for physical metal, and the structure has some quirks worth grasping.

The Goldmoney Holding Explained

The core product is called a Goldmoney Holding. Think of it as an online account where you buy metal, and the company stores the actual bars for you in a vault you select.

There’s no minimum purchase for individual buyers, so you can start small. You fund the account first, then place buy orders at the quoted price. The metal is yours, held on your behalf, not lent out or pooled with a bank’s balance sheet.

Metals on Offer: Gold, Silver, Platinum, Palladium

You can buy and store four metals through a single Holding:

- Gold

- Silver

- Platinum

- Palladium

All four meet recognized delivery standards, which I’ll cover in the vault section. The account supports nine funding currencies, so international buyers aren’t stuck converting to US dollars first.

Allocated vs. Pooled: Why the Distinction Matters

This is the single most important thing to understand. Goldmoney uses allocated storage, meaning specific bars are assigned to you at a 1:1 ratio with the metal in the vault.

Pooled or unallocated storage, common with cheaper providers, means you own a claim against a shared pile the company controls. If that firm fails, you become a creditor.

With allocated metal, the bars are legally yours, not part of the company’s assets. For anyone protecting retirement money, that difference is the whole point.

Getting Started: Account Setup and Verification

Opening a Holding is straightforward on paper, but a couple of steps catch people off guard. Here’s how it actually flows.

The Sign-Up Walkthrough

You create an account online, choose your Holding type, and begin identity verification. The platform blocks buying until you clear at least partial verification and have cash sitting in the account.

The interface itself gets consistent praise for being clean and simple. Setup took most reviewers under an hour, assuming their documents uploaded cleanly the first time.

Identity Checks and the Re-Verification Catch

Goldmoney runs standard KYC identity checks, which is normal and expected for a regulated financial firm. The problem shows up later.

Multiple customers report that previously verified accounts suddenly flip back to “unverified,” forcing them to resubmit documents.

This tends to happen right when someone tries to withdraw, which understandably makes people nervous. It’s the second-most-common complaint I found, and it’s the one that generates the “frozen funds” stories.

Personal, Business, and Trust Holdings

Goldmoney supports more than individual accounts. You can open a Holding as:

- A personal account

- A business or corporate account

- A living or revocable trust

You can also fund from brokerage or joint accounts under certain conditions and link multiple bank accounts. This flexibility makes it usable for estate planning, though trust setups require extra documentation up front.

Funding, Buying, and Payment Methods

Money movement here follows a strict order that trips up first-timers. You can’t buy metal with a card on impulse; you fund first, then purchase.

How Money Goes In

Goldmoney accepts several free funding methods:

- Bank wire

- CHAPS (direct bank transfer)

- SEPA transfers

Funding is free on the Goldmoney side, though your own bank may charge for the wire. The cash lands as a currency balance in your Holding before you can convert it to metal.

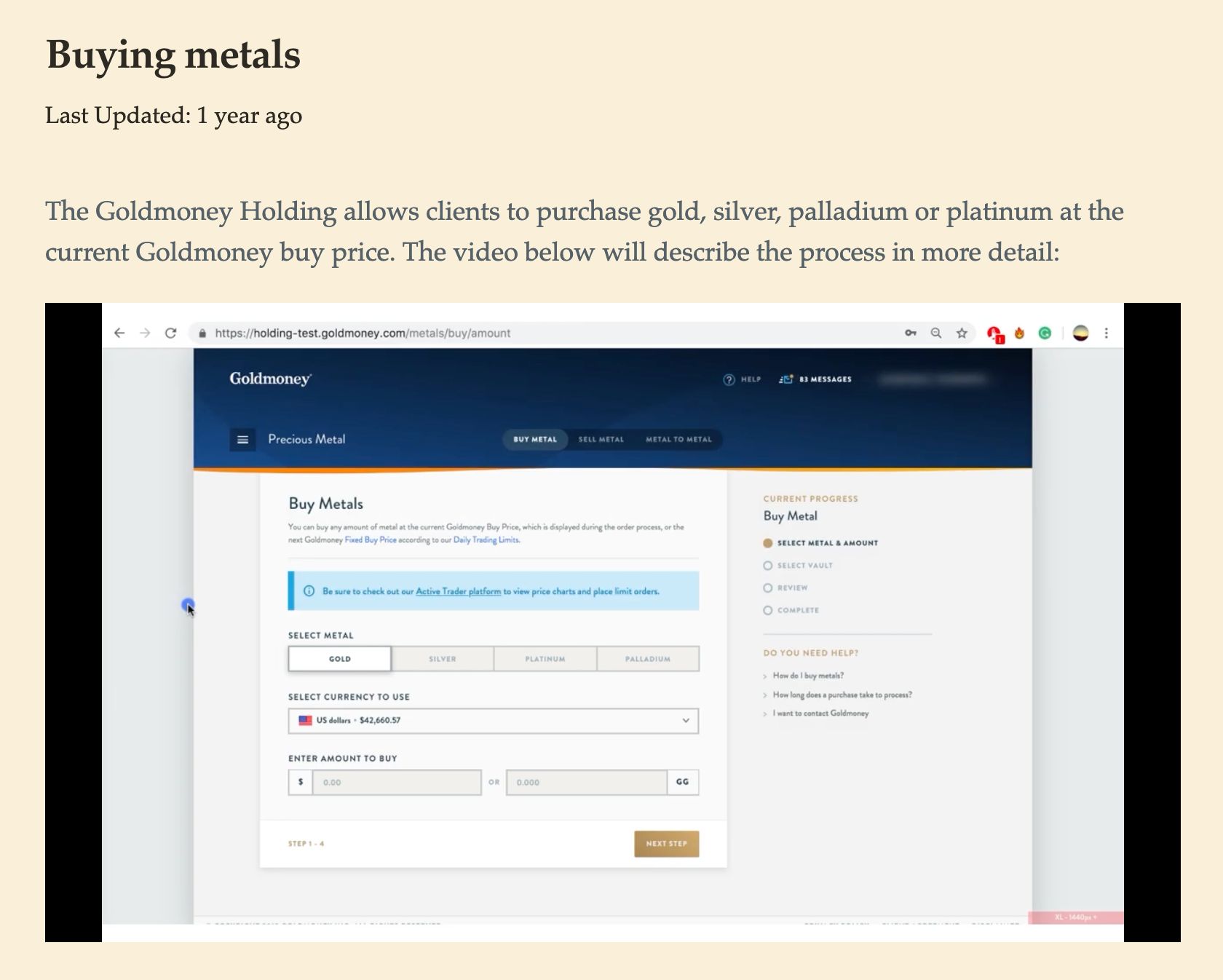

Placing a Buy Order Step by Step

Once your account has a cash balance and verification is complete, buying is quick:

- Confirm your identity checks are finished

- Make sure a currency balance is funded

- Select your metal, vault, and amount

- Place the buy order at the current Goldmoney buy price

- Wait for processing, usually 24 to 48 hours

The price locks in if you confirm within the time window. If the “Buy Metals” button is greyed out, it means either your verification is incomplete or you have no cash sitting in the account.

Where Your Metal Lives: Vaults and Custody Partners

The vault network is where Goldmoney earns its keep. The names behind the storage matter as much as the metal itself.

The Six-Country Vault Network

Goldmoney stores metal in insured vaults across six countries:

- Canada

- Hong Kong

- Singapore

- Switzerland

- United Kingdom

- United States

That’s roughly 13 vaults in total. You pick the location and operator at the moment of purchase, which lets you spread jurisdiction risk or keep metal closer to home.

Loomis, Brink’s, Rhenus, and the Royal Canadian Mint

The actual vaulting is handled by established logistics and security firms, not by Goldmoney itself:

- Loomis

- Brink’s

- Rhenus Logistics

- The Royal Canadian Mint

These are serious names in physical security. Using third-party operators adds a layer of separation between your metal and the company’s corporate finances.

Bar Standards and Serial-Number Registration

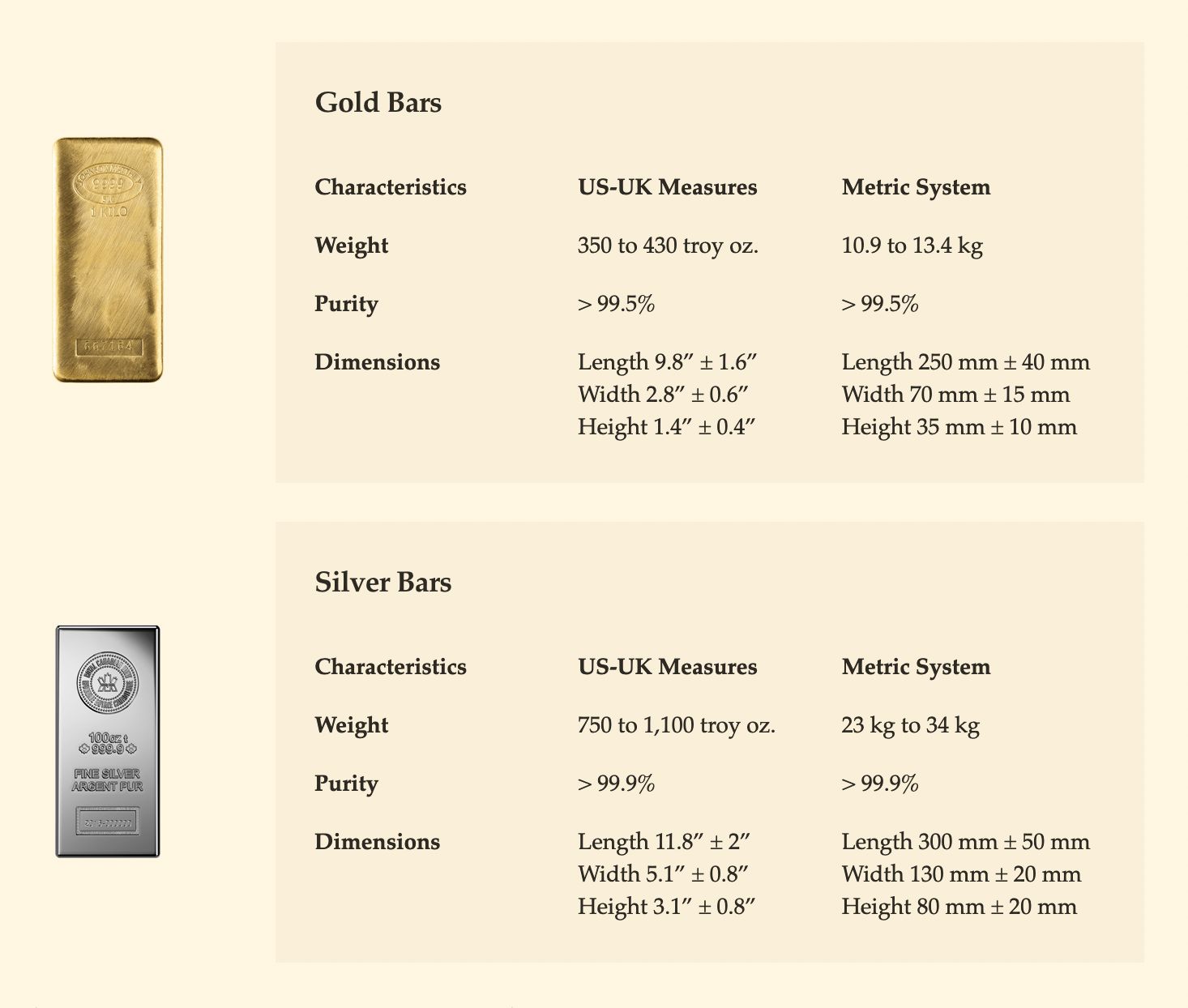

Every bar meets London Good Delivery standards, LBMA for gold and silver and LPPM for platinum and palladium. You can verify what those standards mean directly on the LBMA site.

For a metal fee, you can register a full bar in your own name with its serial number. That turns an abstract claim into a specific, identifiable bar tied to you, which matters if you ever want to redeem physical metal.

Breaking Down the Real Cost of Goldmoney

Fees are where the honest part of this review earns its title. The headline numbers look great; the fine print is where money leaks out.

Buy and Sell Charges

Goldmoney charges a flat 0.5% to buy and 0.5% to sell, per the official fee schedule updated for February 2026. That’s competitive against most physical bullion options.

Some third-party reviews claim the all-in cost of selling runs higher than 0.5% once spreads are factored in, and a few cite an added exchange fee. The official documents state 0.5%, but assume your real round-trip cost lands a bit above the advertised rate.

The Monthly Storage Minimum That Trips People Up

Here’s the trap. Storage runs 0.25% per year on gold, platinum, and palladium, and 0.50% on silver. Reasonable. But there’s a US $10 minimum charge per month regardless of balance.

That minimum is what wrecks small accounts. If you hold $2,000 of gold, $120 a year in storage is a 6% annual drag, far above the advertised 0.25%. The percentage fee only becomes the cheaper option once your balance clears roughly $48,000.

Redemption and Withdrawal Costs

Taking metal out or moving cash carries its own charges:

- Bank wire withdrawals pass through bank fees, roughly $25 USD, £20 GBP, or $35 CAD per wire

- Physical redemption runs 3.00% for gold, 3.80% for silver, 4.70% for platinum, and 5.50% for palladium

- Physical redemption carries a $1,250 USD minimum per request, plus taxes

Physical redemption is expensive by design. Goldmoney is built for storage, not for shipping bars to your basement.

Inactivity and Dormancy Penalties

If you go quiet, the fees escalate. Leave the account untouched and you’ll pay:

- Inactive (3 years without login): a one-time 1.00% plus 1.00% per year

- Dormant (7 years): a one-time 0.75% plus 0.75% per year

Set a calendar reminder to log in at least once a year. These penalties quietly eat into long-term holdings if you forget the account exists.

Cashing Out: Selling, Withdrawing, and Taking Delivery

Buying gold is easy anywhere. Getting your value back out cleanly is the real test of a custody firm, and Goldmoney’s exit paths deserve a close look.

Selling Metal Back on the Platform

There’s no traditional return policy. You sell metal back at the Goldmoney sell price, paying the 0.5% fee, then withdraw the cash to your linked bank account.

Daily client liquidity on the platform provides the pricing, so you’re not waiting for a buyer to appear. In practice, selling is the fast part; withdrawing the cash is where the re-verification snags sometimes surface.

Pulling Out Physical Bullion (and the Minimums Involved)

If you want the actual bars, you can arrange physical redemption or vault pickup. But you have to own enough metal to register a complete bar first, and you’ll pay the redemption percentage plus the $1,250 minimum.

For most holders this route only makes sense with substantial balances. Small buyers are effectively locked into the sell-and-wire path.

Keeping Your Assets Safe

Security is the reason people accept storage fees in the first place. Goldmoney splits protection across the physical vaults and the digital platform.

Vault Insurance and Coverage

Every vault operator insures the stored metal against risks including theft. You can view the actual insurance certificates inside the Governance section of your Holding, which is more transparency than many competitors offer.

Because the metal is allocated and held by third-party vault firms, it sits outside Goldmoney’s corporate balance sheet. If the company hit trouble, your bars would not be counted among its assets.

Platform-Side Protection (Encryption, Account Locks)

On the digital side, the platform uses strong encryption and account-security features:

- AES-256 and RSA-4096 encryption

- Mobile verification

- Account-lock controls

These are bank-grade protections. The irony is that the same security features that keep intruders out are also what trigger the re-verification demands people complain about.

What Real Customers Are Saying

Reviews on Goldmoney are all over the map, and the gaps between platforms tell a story of their own. Reading them side by side reveals more than any single score.

Trustpilot: The 4.2-Star Picture and the Review-Surge Question

On Trustpilot, Goldmoney holds about 4.2 out of 5 across roughly 2,060 to 2,099 reviews. The company replies to around 93% of negative reviews, usually within a week.

One caveat worth flagging: several third-party sources note the Trustpilot score jumped from about 2 stars to 4 stars after a sudden wave of five-star reviews roughly a year ago. Older 2022 snapshots showed averages nearer 2.6. Read the recent reviews with that surge in mind.

BBB: Not Rated, and What That Actually Means

The live Better Business Bureau profile shows Goldmoney as Not Rated, with zero reviews and zero complaints on file. It is not BBB accredited.

Don’t read that as a red flag or a green light. “Not Rated” simply means the BBB lacks sufficient information, not that anything is wrong. Some review sites claim historical complaints, but the current profile shows none.

Sitejabber and Other Voices: The 1.5-Star Reality Check

Then there’s Sitejabber, where Goldmoney scores around 1.5 out of 5 across roughly 91 reviews. That’s a stark contrast to Trustpilot.

The truth probably sits between the two. Sitejabber attracts angrier voices, Trustpilot’s recent surge inflates the positive side, and neither number alone should decide your choice.

The Praise: Relationship Managers and Fast Support

The positive reviews cluster around a few consistent themes:

- Named relationship managers, with Nikita Samant and Ankush Bal praised repeatedly for patience and professionalism

- Fast resolution of withdrawals, verification, and transfers

- Long-term loyalty, with some customers citing 19 to 20 years on the platform

- A smooth, simple user interface

Good customer service and platform usability are the two things happy customers mention most.

The Gripes: Fees, Frozen Funds, and Policy Shifts

The complaints are just as consistent:

- Storage fees introduced on accounts that originally had none

- Verified holdings reverting to unverified, especially during withdrawals

- Poorly communicated policy changes since the 2016 ownership shift

- Serious allegations from some users about account liquidations during closures in early 2025

These aren’t isolated gripes. They repeat across platforms often enough that you should treat them as real risks, not noise.

The Case For and Against Goldmoney

Weighing the evidence, the picture is genuinely mixed. Here’s how the strengths and weaknesses stack against each other.

Where It Genuinely Delivers

Goldmoney does several things well:

- Truly allocated, insured, LBMA-standard metal held by reputable vault operators

- Low buy and sell fees at 0.5% each

- Public TSX listing with audited financials and real transparency

- No minimum purchase and support for nine currencies

- Widely praised human customer support

For low-cost, transparent custody of physical metal, the fundamentals are sound.

The Red Flags Worth Weighing

The concerns are just as concrete:

- The $10 monthly storage minimum that punishes small balances

- Re-verification demands that stall withdrawals

- Expensive physical redemption with a $1,250 minimum

- A history of unpopular post-2016 policy changes

- Wildly inconsistent review scores across platforms

None of these make Goldmoney a scam. They do make it a poor fit for certain buyers.

Who Should and Shouldn’t Use Goldmoney

The right answer depends entirely on your balance and your intentions. Here’s my honest breakdown:

- Good fit: holders with balances above roughly $50,000 who want low-cost, long-term allocated storage and don’t plan to move metal often

- Good fit: international buyers wanting multi-jurisdiction vaulting in a single account

- Poor fit: small savers under $10,000, where the monthly minimum devours returns

- Poor fit: buyers who want cheap physical delivery or frequent trading

- Poor fit: anyone uncomfortable with periodic document re-verification

Match the platform to your situation and the mixed reviews start to make sense. It rewards patient, larger holders and frustrates small, active ones.

Frequently Asked Questions

Q1. Is Goldmoney Safe to Store Thousands of Dollars of Gold With?

Yes, with caveats. Your metal is allocated to you, held by third-party vault operators like Brink’s and Loomis, and insured against theft.

It sits outside Goldmoney’s balance sheet, so a company failure shouldn’t touch your bars. The main risks are operational and jurisdictional, not the loss of the metal itself.

Q2. Why Did My Goldmoney Account Get Flagged for Re-Verification When I Tried to Withdraw?

This is a documented, recurring complaint. Verified holdings sometimes revert to unverified, often right when you attempt a withdrawal, forcing you to resubmit documents.

It’s tied to the platform’s security and compliance systems. Frustrating, yes, but it’s a friction issue rather than evidence your funds are gone.

Q3. Does Goldmoney Actually Charge Only 0.5% When I Sell, or Is It More?

The official fee schedule states 0.5% to sell. Some third-party reviewers argue the real all-in cost runs higher once spreads are included, and a few cite an extra exchange fee. Budget for slightly more than the advertised rate on a full round trip.

Q4. Can I Take Physical Possession of the Gold I Buy on Goldmoney?

Yes, through physical redemption or vault pickup. You must own enough to register a full bar, and you’ll pay 3.00% on gold plus a $1,250 minimum per request, plus taxes. It’s costly, so the platform suits storage far better than home delivery.

Q5. Why Do Goldmoney’s Ratings Differ So Much Between Trustpilot and Sitejabber?

Trustpilot shows about 4.2 stars, boosted by a review surge over the past year, while Sitejabber sits near 1.5. Different platforms attract different crowds, and neither is fully representative. Read recent reviews on both and weigh the specific complaints over the raw average.

My Final Take

Goldmoney is legitimate, transparent, and genuinely useful for the right buyer. I’d trust it with a meaningful gold position if I planned to hold for years and my balance cleared the point where the $10 monthly minimum stops mattering.

I would not use it for a few thousand dollars, and I’d go in fully aware of the re-verification headaches and redemption costs.

If those trade-offs bother you, look at a self-directed gold IRA through a dedicated custodian, or a physical dealer with home storage instead. For low-cost allocated custody from a public company, though, Goldmoney holds up.

Goldco Precious Metals

- Goldco Surpasses $2 Billion in Precious Metals Placements

- Over 6,000 Five-Star Ratings on BBB, Trustpilot, and ConsumerAffairs

- Seven-Time Winer on the Inc. 5000 List